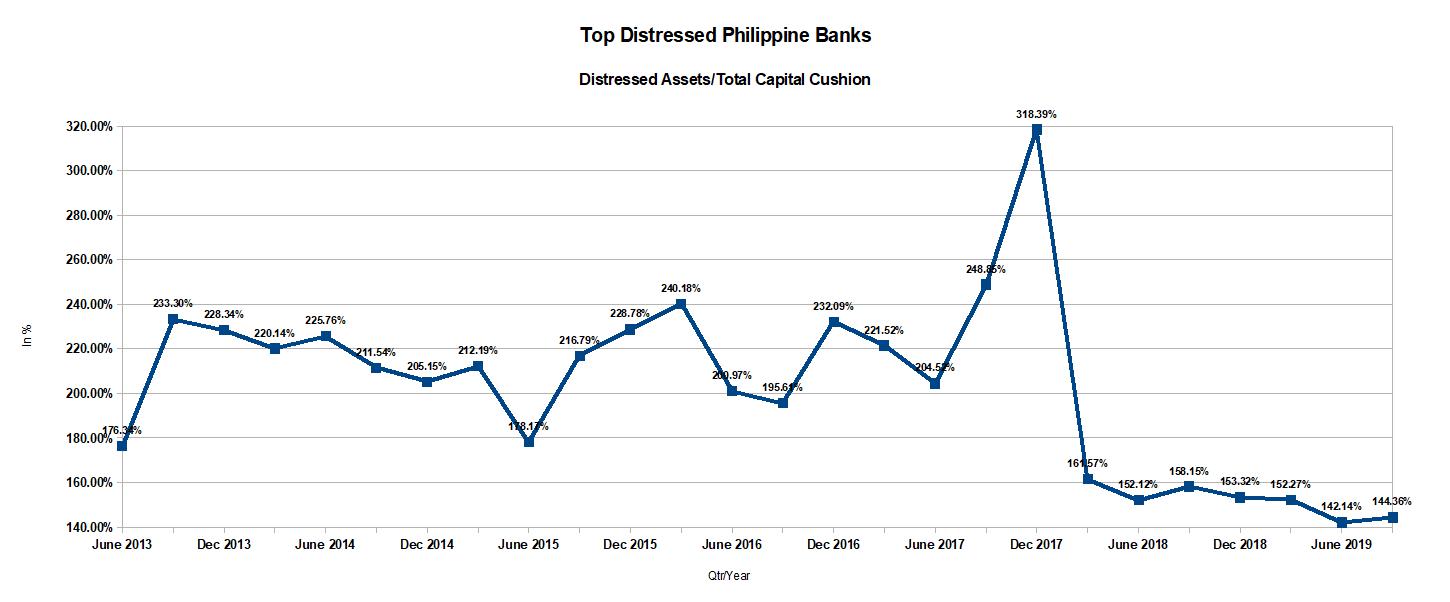

Editor's Note: The ratio of Distressed Assets to Total Capital Cushion is a variant of the famous Texas Ratio, which was widely used by US financial regulators to predict bank failure during the US Savings and Loan Crisis in the 1980s and early 1990s. The basic premise is that a bank with Distressed Assets greater than its Capital Cushion is in danger of insolvency because a significant drop in the value of the Distressed Assets will eat into a significant amount of the bank's capital. A bank that has a Distressed Ratio greater than 100% is flagged as borderline insolvent. For a more detailed discussion of this ratio, please visit a previous blog post: The Texas Ratio of Select Philippine Banks

This is a list of the top distressed Universal and Commercial (U/KB) as well as Thrift Banks in the Philippines as of September 30, 2019. It updates a previous blog post: "The Top Distressed Philippine Banks as of September 30, 2019".

To see where your bank stands relative to these banks, please check the previous blog post: "Philippine Banks Improve Slightly in the 3rd Quarter of 2019 "

| The Top Distressed Philippine Banks | |||

| Total Distressed Assets/ Total Capital Cushion | |||

| September 30, 2019 | |||

| In Php | |||

| September 30, 2019 | |||

| Bank | Total Distressed Assets (In PhP) | Total Capital Cushion (In PhP) | Distressed Assets/ Total Capital Cushion (In %) |

| INTER-ASIA DEVELOPMENT BANK | 603,975,057.13 | 89,057,758.62 | 678.18% |

| RB OF JAEN INC | 289,710,088.82 | 57,795,953.69 | 501.26% |

| SAVIOUR RURAL BANK INC | 520,813,197.77 | 104,266,957.08 | 499.50% |

| RB OF CENTRAL PANGASINAN (BAYAMBANG) INC | 801,173,241.45 | 188,221,990.32 | 425.65% |

| COOP BANK OF CAGAYAN | 383,622,540.56 | 105,371,177.73 | 364.07% |

| RB OF BROOKE'S POINT (PALAWAN) INC | 343,569,235.86 | 98,745,885.41 | 347.93% |

| RB OF DULAG (LEYTE) INC | 351,859,570.12 | 107,563,978.48 | 327.12% |

| BENGUET CENTER BANK INC A RB | 212,938,649.15 | 70,498,979.94 | 302.05% |

| UNITED COCONUT PLANTERS BANK | 18,970,162,725.65 | 6,776,674,065.74 | 279.93% |

| COMMTY RB OF DAPITAN CITY INC | 443,182,863.35 | 161,602,826.39 | 274.24% |

| MALAYAN BANK SAVINGS AND MORT BANK INC | 3,841,811,407.37 | 1,424,236,269.29 | 269.75% |

| RB OF CARDONA (RIZAL) INC | 336,921,658.34 | 125,094,802.07 | 269.33% |

| MAKILING DEVELOPMENT BANK CORPORATION | 909,552,931.50 | 348,548,891.10 | 260.95% |

| VILLAGE BANK INC (A RURAL BANK) | 277,542,111.80 | 107,313,565.81 | 258.63% |

| RB OF MIDSAYAP INC | 229,418,646.01 | 100,925,612.49 | 227.31% |

| RB OF PILAR (BATAAN) INC | 346,780,211.00 | 153,861,114.95 | 225.39% |

| BANK OF CHINA LIMITED-MANILA BRANCH | 21,277,361,603.71 | 10,086,765,483.16 | 210.94% |

| PLANBANK "RB OF CANLUBANG PLANTERS INC" | 310,188,918.31 | 154,423,979.91 | 200.87% |

| YUANTA SAVINGS BANK PHILIPPINES INC | 1,651,442,735.73 | 904,821,958.20 | 182.52% |

| RANG-AY BANK INC (A RURAL BANK) | 945,625,397.50 | 533,212,561.60 | 177.34% |

| RB OF GENERAL TRIAS INC | 230,627,278.26 | 141,763,762.14 | 162.68% |

| AMA RURAL BANK OF MANDALUYONG INC | 1,403,596,530.43 | 891,921,691.66 | 157.37% |

| RB OF SAN LUIS (PAMPANGA) INC | 175,464,578.25 | 114,537,220.96 | 153.19% |

| ENTERPRISE BANK INC (A THRIFT BANK) | 615,972,133.84 | 416,558,371.02 | 147.87% |

| RB OF SAN MATEO(ISABELA) INC | 193,132,656.41 | 136,654,395.35 | 141.33% |

| PEOPLES BANK OF CARAGA INC (A RURAL BANK) | 591,956,730.74 | 421,692,152.80 | 140.38% |

| EQUICOM SAVINGS BANK INC | 1,342,600,228.77 | 1,046,369,742.58 | 128.31% |

| RB OF BAMBANG (NUEVA VIZCAYA) INC | 176,270,866.46 | 138,079,267.69 | 127.66% |

| COUNTRY BUILDERS BANK INC (A RURAL BANK) | 447,566,361.42 | 354,184,625.30 | 126.37% |

| RB OF MARIA AURORA (AURORA) INC | 296,616,768.80 | 238,942,441.99 | 124.14% |

| RB OF BAYOMBONG INC | 222,900,266.96 | 181,010,882.20 | 123.14% |

| CHINA BANK SAVINGS INC | 14,333,672,582.61 | 11,704,604,899.76 | 122.46% |

| COMMON WEALTH RURAL BANK INC | 158,816,261.60 | 133,847,522.75 | 118.65% |

| COOPERATIVE BANK OF BOHOL | 128,504,467.96 | 112,434,247.74 | 114.29% |

| UCPB SAVINGS BANK | 3,990,723,671.68 | 3,581,278,919.06 | 111.43% |

| PHIL BANK OF COMMUNICATIONS | 14,133,443,495.97 | 12,760,687,633.53 | 110.76% |

| GATEWAY RURAL BANK INC | 134,585,785.25 | 122,636,282.32 | 109.74% |

| CORDILLERA SAVINGS BANK INC | 150,654,300.79 | 137,457,221.38 | 109.60% |

| GM BANK OF LUZON INC (A RURAL BANK) | 524,403,298.67 | 483,172,924.10 | 108.53% |

| RB OF SAN NARCISO INC | 58,771,706.43 | 55,716,472.11 | 105.48% |

| PRODUCERS SAVINGS BANK CORPORATION | 2,393,150,809.36 | 2,271,730,683.32 | 105.34% |

| ASIA UNITED BANK CORPORATION | 31,993,330,514.85 | 30,654,018,442.84 | 104.37% |

| Grand Total | 126,744,414,086.64 | 87,798,303,614.58 | 144.36% |

Source: www.bsp.gov.ph

Disclaimer:

This list only serves as a screening guide. It is not a definitive guide and must be taken in the context of other factors. The figures are based on the individual banks' statement of condition as of June 30, 2019 and September 30, 2019 as published in the BSP website (www.bsp.gov.ph). For this analysis, no attempt was made to go through the audited financial statements of each bank. Readers are suggested to make their own investigations and verify the figures presented. Both BSP and PDIC have their own problem bank screening systems that are much more sophisticated in scope and design, given that they have more access to information over the banks they regulate.

No comments:

Post a Comment